| From |

12.01am 30 March 2022 |

There are a few jokes going around social media about the price of fuel.

As widely predicted, the Government will temporarily reduce the excise and excise-equivalent customs duty rate that applies to petrol and

diesel by 50% for 6 months from Budget night. That is, the current 44.2 cents per litre excise rate will reduce to 22.1 cents per litre from

Budget night. However, the measure is subject to the passage of the enabling legislation so don’t expect to see a change right away.

The reduction extends to all other fuel and petroleum based products except aviation fuels.

At the conclusion of the 6 months on 28 September 2022, the excise and excise-equivalent customs duty rates revert to previous rates including any indexation that would have applied during the 6 month period.

The Australian Competition and Consumer Commission (ACCC) will monitor the price behaviour of retailers to ensure that the lower excise rate is passed on to consumers.

The measure comes at a cost of $5.6bn.

| From |

1 July 2021 to 30 June 2022 |

The low and middle income tax offset (LMITO) currently provides a reduction in tax of up to $1,080 for individuals with a taxable income of

up to $126,000.

The tax offset is triggered when a taxpayer lodges their 2021-22 tax return.

For the 2021-22, the LMITO will be increased by $420 which means that the proposed new rates for individuals are as follows:

| Taxable income |

Offset |

| $37,000 or less |

$675 |

| Between $37,001 and $48,000 |

$675 plus 7.5 cents for every dollar above $37,000, up to a maximum of $1,500 |

| Between $48,001 and $90,000 |

$1,500 |

| Between $90,001 and $126,000 |

$1,500 minus 3 cents for every dollar of the amount above $90,000 |

| From |

April 2022 |

A one-off $250 ‘cost of living payment’ will be provided to Australian resident recipients of the following payments and concession card

holders:

The payments are exempt from taxation and will not count as income support for the purposes of any income support payment. An individual can only receive one payment.

| From |

1 July 2021 |

The Medicare levy low income thresholds for seniors and pensioners, families and singles will increase from 1 July 2021.

| |

2020-21 |

2021-22 |

| Singles |

$23,226 |

$23,365 |

| Family threshold |

$39,167 |

$39,402 |

| Single seniors and pensioners |

$36,705 |

$36,925 |

| Family threshold for seniors and pensioners |

$51,094 |

$51,401 |

For each dependent child or student, the family income thresholds increase by a further $3,619 instead of the previous amount of

$3,597.

The Home Guarantee Scheme guarantees part of an eligible buyer’s

home loan, enabling people to buy a home with a smaller deposit and without the need for lenders mortgage insurance. The Government has

extended two existing guarantees and introduced a new regional scheme.

Just prior to the Budget, the Government announced:

|

Resources |

| From |

1 July 2024 |

Trust and beneficiary income reporting and processing will be digitalised with all trusts being provided with the option of lodging income

tax returns electronically.

While this measure will reduce compliance costs, it will also increase transparency and provide the ATO with a greater insight into where

anomalies are occurring.

The temporary 50% reduction in superannuation minimum drawdown requirements for account-based pensions and similar products has been extended to 30 June 2023.

Minimum superannuation drawdown rates 2019-2023

| Age |

Default minimum drawdown rates (%) |

Reduced rates by 50% for the 2019-20 to 2022-23 income years (%) |

| Under 65 |

4 |

2 |

| 65-74 |

5 |

2.5 |

| 75-79 |

6 |

3 |

| 80-84 |

7 |

3.5 |

| 85-89 |

9 |

4.5 |

| 90-94 |

11 |

5.5 |

| 95 or more |

14 |

7 |

| From |

7:30pm AEDT, 29 March 2022 until 30 June 2023 |

The Government intends to provide a 120% tax deduction for expenditure incurred by small businesses on business expenses and depreciating

assets that support their digital adoption, such as portable payment devices, cyber security systems or subscriptions to cloud based

services.

The technology boost will be available to small business with an aggregated annual turnover of less than $50 million.

An annual expenditure cap of $100,000 will apply to the boost.

The boost for eligible expenditure incurred by 30 June 2022 will be claimed in tax returns for the following income year. The boost for eligible expenditure incurred between 1 July 2022 and 30 June 2023 will be included in the income year in which the expenditure is incurred. That is, the additional deduction available under this measure is expected to be claimed in the 2023 tax return.

Resources

|

| From |

2022-23 income year |

Normally, GST and PAYG instalment amounts are adjusted using a GDP adjustment or uplift. For the 2022-23 income year, the Government is

setting this uplift factor at 2% instead of the 10% that would have applied.

The 2% uplift rate will apply to small to medium enterprises eligible to use the relevant instalment methods for instalments for the 2022-23 income year and are due after the amending legislation comes into effect:

|

Resources |

In broad terms, an Employee Share Scheme (ESS) is a scheme under which shares in a company, or rights to acquire shares in a company, are issued to an employee or their associate in respect of their employment.

At a commercial level, ESS arrangements are often used to better align the interests of employers and employees, as employees are provided with an opportunity to share in the profitability and growth of the business. The arrangements can also be useful in situations where a business is in start-up mode and does not have significant cash flow or reserves to attract top quality employees with high salaries.

The Government has flagged changes to the ESS rules to expand access to schemes so that employees at all levels can directly share in the growth of the business.

Where employers make larger offers in connection with employee share schemes in unlisted companies, participants can invest up to:

The Government will also remove regulatory requirements for offers to independent contractors, where they do not have to pay for interests.

While these changes might expand access to employee share schemes, it is important to consider the tax implications that can arise for employee when they receive shares or options at a discount to their market value. There are a number of different ways that employees can be taxed in this area and the treatment will often depend on how the ESS arrangement has been structured by the company.

The Patent Box tax regime was announced in the 2021-22 Budget for the medial and biotech industries and provides a concessional effective corporate tax rate of 17% on income derived from patents, to the extent that the taxpayer undertakes the R&D of that patent in Australia.

The Government has announced an extension of the regime to:

Note that the legislation enabling the original 2021-22 Budget measure has not been enacted and is currently before Parliament – see Treasury Laws Amendment (Tax Concession for Australian Medical Innovations) Bill 2022.

Emissions reduction

| From |

Patents granted after 29 March 2022 Income years starting on or after 1 July 2023 |

Applies to patents relating to low emissions technology, as set out in the 140 technology areas listed in the Government’s 2020

Technology and Investment Roadmap Discussion Paper

or included as priority technologies in the Government’s 2021 and future annual Low

Emissions Technology Statements,

provided the patented technology is considered to reduce emissions.

Agricultural sector

| From |

Patents granted after 29 March 2022 Income years starting on or after 1 July 2023 |

Applies to corporate entities that commercialise their eligible patents linked to agricultural and veterinary (agvet) chemical products

listed on the Australian Pesticides and Veterinary Medicines Authority (APVMA), PubCRIS

(Public Chemical Registration Information System) register, or eligible Plant

Breeder’s Rights

(PBRs).

Medical and biotechnology innovations updated

Since the original announcement, the Government has made two

significant expansions to the patent box regime:

Taxpayers will still only benefit from the concessional tax treatment under the patent box to the extent that the R&D occurred in Australia.

|

Resources |

| From |

1 July 2023 |

From 1 July 2023, fuel and alcohol businesses with an annual turnover of less than $50 million will be able to lodge and pay excise and

excise equivalent customs duty on a quarterly basis, rather than weekly or monthly. These businesses will lodge returns and pay excise by

the 28th day of the month after the end of each quarter.

In addition, businesses that import fuel and alcohol products for further manufacture or distribution, and want to defer payment of excise or excise-equivalent customs duty, will be able to transfer the fuel or alcohol straight into a warehouse administered by the ATO once the products have gone through Australian Border Force (ABF) customs clearance. The ABF will still collect tax on direct imports.

Licensing requirements across the excise system will also be streamlined by:

And, the excise and excise-equivalent customs duty regime for fuel will be amended by:

The excise law will be amended to provide a targeted exemption from excise licensing requirements, up to a threshold of 10,000 litres per year, for licensed hospitality venues to fill beer from kegs into sealed, non-pressurised containers of no more than 2 litres capacity and not designed for medium to long term storage (‘growlers’).

| From |

1 July 2022 |

The sale of Australian Carbon Credit Units (ACCUs) and biodiversity certificates generated from on-farm activities to be treated as primary

production income for the purposes of the Farm Management Deposits (FMD) scheme and tax averaging from 1 July 2022.

In addition, the taxing point of ACCUs for eligible primary producers will change to the year when they are sold, and similar treatment will be extended to biodiversity certificates issued under the Agriculture Biodiversity Stewardship Market scheme, from 1 July 2022. Currently, ACCU holders are taxed based on changes in the value of their ACCUs each year, which can result in tax liabilities prior to sale. Eligible primary producers are those who are currently eligible for the FMD scheme and tax averaging.

| From |

1 July 2022 |

The temporary tariff concession in place for certain medical and hygiene products to treat, diagnose or prevent the spread of COVID 19 will

be made permanent and the range of products to which the concession applies expanded.

| From |

1 January 2024 |

As announced prior to the Budget, companies will be able to choose to have their pay as you go (PAYG) instalments calculated using current

financial performance, extracted from business accounting software, with some tax adjustments.

The move is intended to ensure that instalment liabilities are aligned to the businesses cashflow. In addition, the digitisation of PAYG instalments will improve transparency and provide more accurate data on performance.

|

Resources |

| From |

1 January 2024 |

As announced prior to the Budget, businesses will be able to report Taxable Payments Reporting System data via their accounting software on

the same lodgment cycle as their activity statements.

The measure is expected to reduce the costs of complying with the system and increase transparency.

As announced prior to the Budget, the Government will commit $6.6 million for the development of IT infrastructure that will enable the ATO to share Single Touch Payroll (STP) data with State and Territory Revenue Offices on an ongoing basis.

The funding will be deployed following further consideration of which states and territories are able and willing to make investments in their own systems and administrative processes to pre-fill payroll tax returns with STP data in order to reduce compliance costs for businesses.

| From |

1 July 2022 |

Back in the 2019-20 Budget, the Government announced that Australian Business Number (ABN) holders would be stripped of their ABNs if they

failed to lodge their income tax return. In addition, ABN holders would be required to annually confirm the accuracy of their details on the

Australian Business Register.

This measure has been deferred for 12 months, which means that the tax return lodgement obligation is due to commence from 1 July 2022 with the annual confirmation of ABN details to commence from 1 July 2023.

The measure that enables payments from certain state and territory COVID-19 business support programs to be treated as non-assessable non-exempt (NANE) income has already been extended until 30 June 2022.

The Government has announced that the following state and territory grant programs have been made eligible for this treatment since the 2021-22 MYEFO, although it is not clear whether the relevant legislative instruments have been issued as yet:

This builds on the list of existing grants paid by New South Wales and Victoria that can already qualify for NANE income treatment.

| From |

1 July 2021 |

As previously announced, work‑related COVID‑19 test expenses incurred by individuals will be made tax deductible.

Changes will also be made to ensure that FBT will not be payable by employers if they provide fringe benefits relating to COVID‑19 testing to their employees for work‑related purposes.

The changes for deductions will be effective from 1 July 2021, with the FBT changes to apply from 1 April 2021.

At this stage it is not entirely clear whether the deduction rules will cover expenses incurred where the employee is able to work from home. The initial media release indicates that the measure will cover situations where the individual has the option of working remotely, while the Budget only refers to costs of taking a COVID-19 test to attend a place of work but doesn’t specifically refer to employees who can work from home.

Resources

|

| From |

7:30pm AEDT, 29 March 2022 until 30 June 2024 |

The Government intends to provide a 120% tax deduction for expenditure incurred by small businesses on external training courses provided to

employees. The deduction will be available to small business with an aggregated annual turnover of less than $50 million. External training

courses will need to be provided to employees in Australia or online, and delivered by entities registered in Australia.

Some exclusions will apply, such as for in-house or on-the-job training and expenditure on external training courses for persons other than

employees.

We assume there will need to be a nexus between the employee’s employment and the training program undertaken for the boost, although we are waiting on further details of this initiative to be released.

The boost for eligible expenditure incurred by 30 June 2022 will be claimed in the tax return for the following income year (that is, the 2023 tax return). The boost for eligible expenditure incurred between 1 July 2022 and 30 June 2024, will be included in the income year in which the expenditure is incurred.

Resources

|

Just prior to the Federal Budget, the Government announced the extension of the:

Any employer (or Group Training Organisation) who takes on an apprentice or trainee up until 30 June 2022 can gain access to:

|

Resources |

The pandemic has created a scarcity of labour. As a result, the Government is relaxing certain work restrictions for a range of visas including eligible Student and Working Holiday Maker (WHM) visa holders, and extended visas for certain engineering graduates negatively affected by COVID-19 travel restrictions.

International students and WHM visa holders who bring forward their arrival to Australia will be refunded the Visa Application Charge for Student visa holders who arrive in Australia between 19 January 2022 and 19 March 2022, and for WHM visa holders who arrive in Australia between 19 January 2022 and 19 April 2022, inclusive.

And, the Government will also increase country caps for Work and Holiday visas by 30% in 2022-23, increasing overall places available by around 11,000.

The Government has stated that it will also “clarify the tax treatment for income earned by workers under the Australian Agriculture Visa scheme established in MYEFO 2021-22 to respond to workforce shortages in the agriculture and primary industry sectors.” At this stage, we don’t know what this clarity means!

An additional $652.6m has been set aside to extend the ATO’s Tax Avoidance Taskforce by 2 years to 30 June 2025.

In that time, the taskforce is expected to increase receipts by $2.1bn and increase payments by $652.6m.

Buried under the wildly exciting headline of Commonwealth’s Deregulation Agenda, is the $19.9 million spend by the Australian Bureau of Statistics to develop a new reporting application to enable businesses to submit surveys on business indicators directly through their accounting software. Excellent. Real time reporting utilising verified data on the state of Australian business.

$446.1 million over 5 years has been provided to increase energy security, maintain affordable and reliable power for households and

businesses and reduce the cost of deploying low emissions technologies. $247m of that is to support increased private sector investment in

low emissions technologies including hydrogen, the continued development of a hydrogen Guarantee of Origin scheme, and the development of a

Biodiversity Stewardship Trading Platform to support farmers to undertake biodiversity activities ahead of the introduction of a voluntary

biodiversity stewardship market.

Another $148.6m is for the development of community microgrids and just over $50m to develop gas infrastructure projects.

|

Resources |

The Government will provide $1.3 billion from 2021-22 to grow the Australian space sector and space manufacturing industry. This includes $1.2bn to establish a National Space Mission for Earth Observation to secure access to key earth observation data streams, build Australia’s sovereign capability and enter agreements with international partners including for the procurement and operation of Australian Satellite Cross Calibration Radiometer satellites. And, $65.7m to fast track the launch of space assets.

Resources

|

For those of you who have been watching the reaction to the Solomon Islands security agreement with China, the appearance in the Budget of infrastructure investment in the Pacific will come as no surprise.

The Government will increase the Australian Infrastructure Financing Facility for the Pacific to $3.5 billion, supporting additional infrastructure investment in the Pacific. This includes projects in Papua New Guinea to improve roads and power. An additional $650m will provided as a loan for PNG’s COVID-19 recovery.

$245.5m will be spent over 5 years on the partnership with India. A new Chancery for the Australian High Commission in Honiara. And, $324.4m to Pacific Island countries and Timor Leste to support their COVID-19 recovery.

Just prior to the Budget’s release, the Government announced $17.9bn in new and additional funding for existing infrastructure projects. Full details of infrastructure funding are on the Infrastructure Investment Program website.

Australian Capital Territory

New projects:

New South Wales

New projects:

Additional funding for existing projects:

Northern Territory

New projects:

Queensland

New projects:

Additional funding for existing projects:

South Australia

New projects:

Additional funding for existing projects:

Tasmania

New projects:

Victoria

New projects:

Additional funding for existing projects:

Western Australia

New projects:

Additional funding for existing projects:

Australia’s unemployment rate is at 4%: the lowest rate in 48 years.

Amid the ongoing COVID 19 pandemic and natural disasters, the Australian economy has outperformed all major advanced economies, experiencing

a stronger recovery in output and employment from pre pandemic levels. The recovery is expected to continue with the unemployment rate

forecast to reach 3.75% in the September quarter of 2022, nearly 3% below the forecast 2 years ago.

The Wage Price Index (WPI) is forecast to increase from 2.75% through the year to the June quarter of 2022 to 3.25% through the year to the June quarter of 2023. But, there is “significant uncertainty around the pace at which wages growth will accelerate.”

Real GDP is forecast to grow by 4.25% in 2021‑22. And, by 3.5% in 2022‑23 and 2.5% per cent in 2023‑24.

The deficit for 2022‑23 is expected to be $78 billion or 3.4% of GDP.

Since the Mid Year Economic and Fiscal Outlook (MYEFO), the underlying cash balance has improved by $103.6 billion over the 5 years to 2025-26. The Budget shows the deficit more than halving to 1.6% of GDP by 2025-26 before falling to 0.7% of GDP by the end of the medium term. Gross debt as a share of the economy is expected to peak at 44.9% of GDP at 30 June 2025, 5.4% lower and 4 years earlier than projected at MYEFO. Gross debt is projected to fall to 40.3% of GDP by the end of the medium term, 9.6% or $236 billion lower than at the end of the medium term in MYEFO.

The Budget projects a halving in the deficit to 1.6% of GDP by 2025‑26 before falling to 0.7% of GDP by the end of the medium term.

Commodity prices are near record high levels, in part due to the Russian invasion of Ukraine. Metallurgical and thermal coal spot prices have recently reached highs that are 62% and 53% above previous peaks.

Inflation is expected to rise to 4.25% through the year to the June quarter of 2022. This reflects higher global oil prices and ongoing supply chain pressures as well as price pressures in the housing construction sector. Then moderate to 3% in 2022‑23 and 2.75% in 2023‑24.

The recent floods in Queensland and New South Wales have had a devastating impact on many communities. The Government expects to spend over $6 billion in total on disaster relief and recovery (in addition to the $3.6 billion already allocated to households, businesses and communities).

On COVID-19, the Budget assumes:

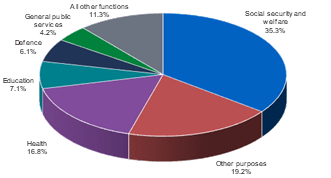

As the Government’s response to the COVID-19 pandemic reduces, expenses decrease from $640 billion in 2021-22 to $628 billion in 2022-23 –

an impact that is primarily reflected in the health, social security and welfare, and other economic affairs functions. Expenses are

expected to reach $687 billion in 2025-26. While, low unemployment and increased economic growth has reduced expenditure on income support

programs, higher inflation and wages growth forecasts have impacted indexation rates and led to increased expenditure estimates on

government payments to individuals.